A budget is the most personal thing you will ever create. It’s honestly a reflection of your life, your wants, your goals, and your dreams. Not only that, but your budget can tell you some pretty incredible things about your money.

The process of closing out your budget (figuring out where your money went during the month) is so important. It’s going to show you where your money went, what categories you should be using in your budget and for your cash envelopes, and how much to assign for your budget categories realistically.

It will also show you if your spending is aligning with your financial goals, and what progress you are making. Don’t just blindly follow a budget. Understand the reasons behind your financial choices, and look at what your budget tells you.

MY APRIL 2019 BUDGET RECAP

WHERE DID MY MONEY GO?

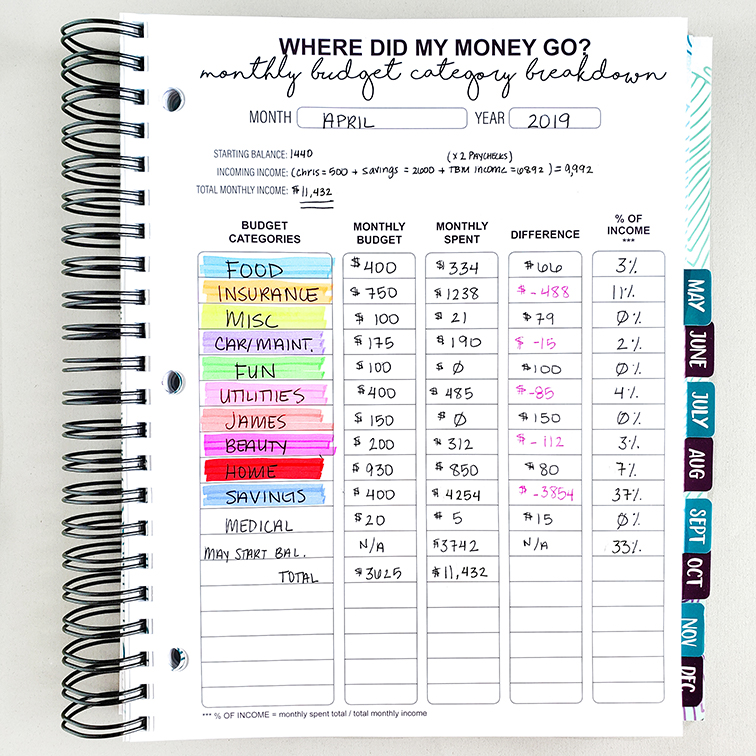

At the end of every month, I take all of the information from my expense trackers, and I organize my spending into categories. Now, I have been budgeting for a very long time, so I use the same categories over and over. If you are just starting out, organizing your spending into categories that make sense to your life, might take some time and tweaking.

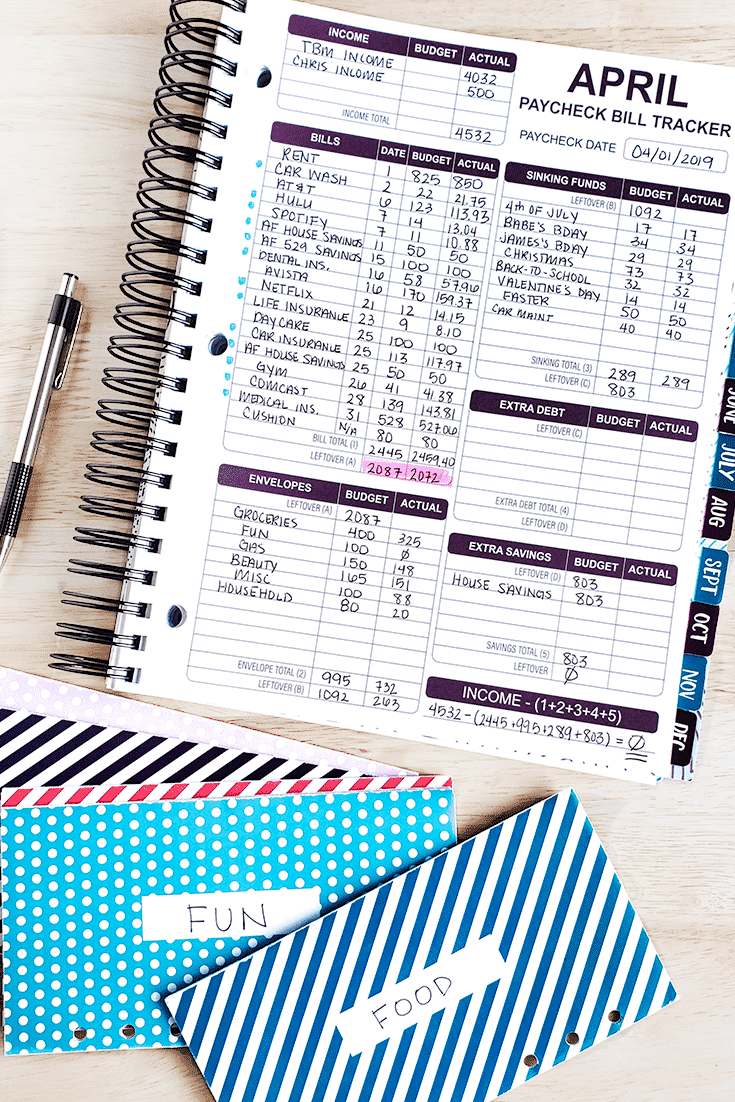

I track my budget from the first of every month to the last day of the month.

Even though I budget my income by paycheck, I still like to assign a monthly budget for each one of my categories. For April 2019, my most significant expense was savings. 37% of my income went towards my savings goals.

This is my third month budgeting my money only once a month. The transition has been a lot easier than I thought, and I am still succeeding with the cash envelope method.

I did not complete meal planning in April, but still managed to stay under budget. I really focused on eating what we already have at home and watched my spending closely for my other categories.

My utility costs were very high this month. My laptop was stolen in early February, so I had to change my bank accounts. During the process, I forgot to change my payment information for my utility payment, so it was drafted in the early part of April. That means my utility bill is showing up twice for this month.

I also completed the $10 Cash Envelope Savings Challenge, and it was a huge success! For the challenge, I saved $60 from my cash envelopes. I put that money towards my house savings goal.

I like to know if I was over or under my monthly budget. If I was over, I mark that amount with a “+” sign and write it in black. If I came under budget, I mark it with a “-” sign and write it in red. This allows me to see how I did with overspending.

I use a zero-based budget, which means my “budget” is really just a sum of my income. So some months, my income decreases or increases. My spending will always reflect those fluctuations.

- Read: March 2019 Budget Recap

THE STARTING BALANCE

A starting balance is something that will always be listed on my budget recaps. I like to keep extra money in my checking account at all times, which I call my “checking account cushion.” When you are working with a zero-based budget, all of your income is essentially being used. If you are using a zero-based budget correctly, that means you should have no money left in your checking account, because it should all have a plan for your spending on your budget.

When I first started using the zero-based budget, the idea of bringing my checking account down to $0 every month freaked me out. My cushion allows me to have extra money just in case a bill is higher than expected, or I have an unexpected expense that I need to cover. I also use my cushion for any unanticipated online purchases that I make, and then I replenish my cushion using the cash I have from my envelopes.

Some people call their starting balance “savings” or “beginning balance” but I have it labeled in my worksheets as “starting balance.”

Do you use the last paycheck of every month to cover some of the bills for the beginning of the next month? For example, your January 20th paycheck will be used to pay for some bills on February 1st, like rent. By carrying over this starting balance into the new month, you will have the income to cover those expenses.

For my monthly income, I use starting balance plus incoming income.

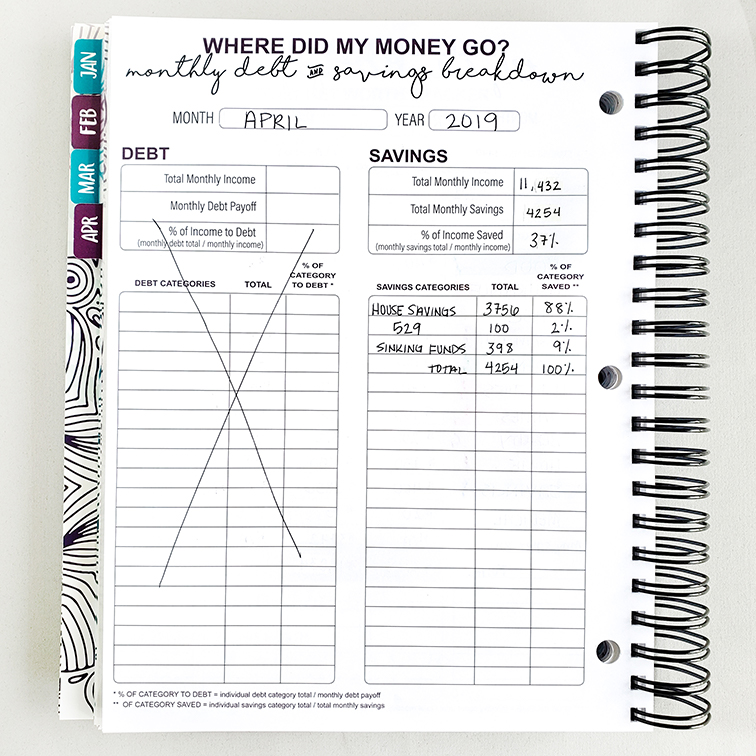

HOW MUCH WENT TO DEBT AND SAVINGS

I like to keep track of my financial goals. Yes, it’s nice to know how much went to savings for the entire month, but I want to know what am I saving for. What savings goals am I currently spending my money on?

Same with debt. I don’t want to know how much total went to debt during the month, but what specific debts am I paying off?

$4,254 (or 37%) of my monthly income went towards savings in April. Out of the $4,254 that I saved, 88% went towards my house savings account.

I left my full-time job in February to work for my business full time. After leaving, I had to plan out how I was going to save for retirement. I decided to create a 401(k) for my business, and April was the first month that I made a contribution. Even though I will not include my 401(k) contributions on my “Where Did My Money Go?” Worksheets, I will be keeping track of my retirement balance on my Yearly Balance Tracker.

Now that I am debt free, I have decided to make saving for my son's future more of a priority. I have set up a 529 College Savings account and will now contribute $100 every month to his account.

In April, all of my leftover cash from my envelopes went towards my house savings goal. Usually, I dedicate that income to my Disneyland trip savings account, but we have decided to push our trip to February 2020, so I contributed a lot less to this savings goal.

I use sinking funds in my budget to help me save for the future. You can read about why you should start using sinking funds in this article. In March, I added more sinking funds to my budget, so I have the cash to cover future holidays, events and occasions happening in 2019.

I also have a car maintenance savings account, which is a separate savings account at my credit union. I usually contribute $40 every month to this account, but forgot to do so in April. I will make up for that mistake in May and June.

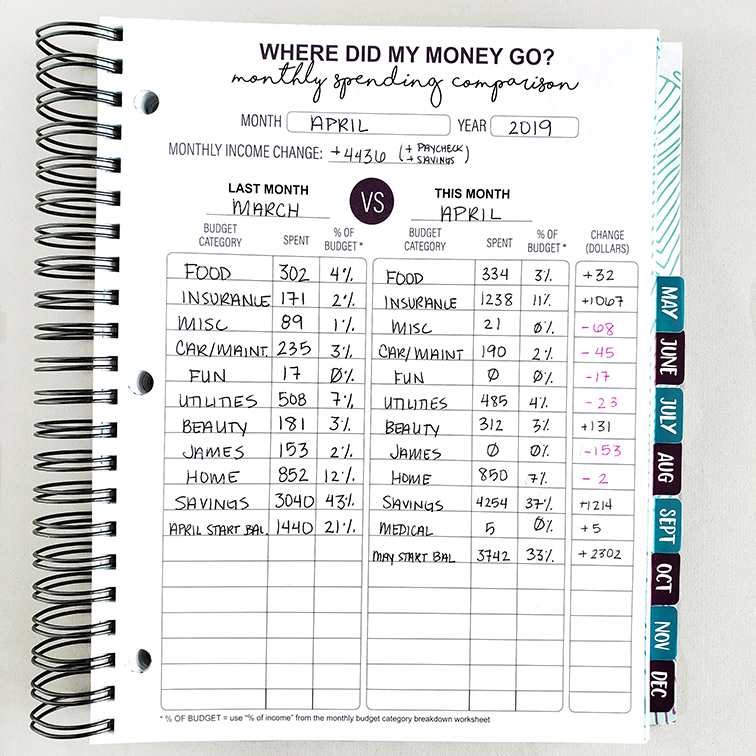

HOW DID MY SPENDING COMPARE TO LAST MONTH

Every month, I like to look at how my spending compared to the previous month. It helps me answer the question, “Did I make progress or decrease my spending in certain categories?”

The one category I am always fighting is my food budget. This is the one category I like to look at. I always try to challenge myself to spend less, and I want to make sure that my spending is going down or staying the same from month-to-month, not increasing.

If your income fluctuates every month like mine does, it’s also an excellent way to see where you are compensating in your spending for those fluctuations. For example, in April my income increased by $4,436. The question I like to answer is, “if my income increased in April, where did my extra income go to compensate for that increase?”

For the change in dollars, I write it in red if I spent less than the previous month, and I write in black if I spent over what I spent in the last month.

My April income was very high. I had a trip planned for New York on May 2nd, and I wanted to make sure my finances were taken care of before I left on my trip. I decided to cash my paycheck on April 30th, rather than May 1st, so April was a two paycheck month. I am still paying all of my May expenses with the paycheck I deposited in April, but I have decided to count it as April income.

I also transferred $2,600 from my house savings account to my checking account so I could write a check to my investment account. I counted this deposit into my checking account as income for April.

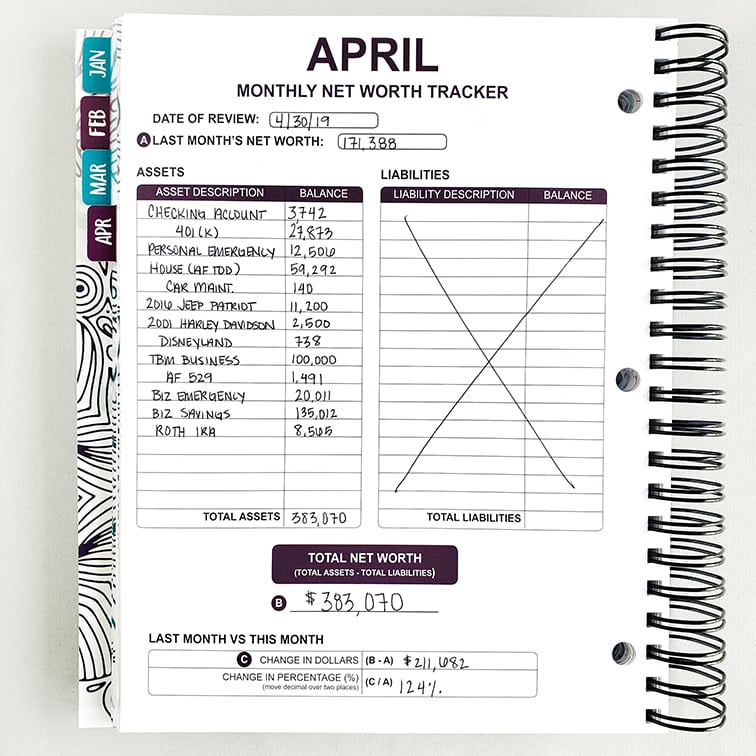

MY NET WORTH

One of the things that a lot of people don't consider when looking at their finances is their net worth.

Your net worth is an overall picture of your financial health, and it can tell you if you are making progress. Your net worth is your total assets minus your total liabilities. The goal of your net worth should be to increase it every month.

You need to increase your assets (saving money), or you need to decrease your liabilities (paying off debt). As you get older, you want your net worth to increase.

At the beginning of 2018, I started out with negative net worth. I owed more than I owned. I made it a goal to have a net worth of $100,000 by the end of 2018. That means I focused on saving money and paying off my debt.

In April my Net Worth increased significantly. It increased by 124%. After four months of not saving for my house goal, I decided to use business income to make a $50,000 contribution to my house savings investment account. Currently, the money that I am saving for my house is invested in mutual funds.

- Watch on YouTube: What Is Your Net Worth & Why Does It Matter?

![]()

Currently, I have $59,292 saved for my house. Only $340,708 left to go. Using a savings trackers like the one shown, is just one of the ways I stay motivated for long-term financial goals. It will be years before I can buy my first home with cash, but seeing the progress pushes me to keep going. You can find this free house savings tracker in the Free Resource Library.

MY APRIL 2019 BUDGET RECAP

I made a lot of progress in April, and I am very excited to see my growth in 2019.

There are two fundamental things that I have learned on my financial journey.

One. There is no wrong or right way to budget your money. The right way is the way that works for you. It doesn't matter what the financial experts are out there telling you or what you might be reading about budgeting. You have to do what works for you and your unique life.

I get asked all the time why I choose to save money while I am on a debt payoff journey. I get judged a lot because it's not what Dave Ramsey would do. So my simple answer – it works for me and my financial goals. Don't be afraid to budget outside of the box, and do things that you feel are right for you and your family.

Two. Being on a debt free journey doesn't just mean making debt payments. Your budget is just as important as paying off debt. It's about having a system in place to ensure that you don't go into debt in the future. What are you doing today with your money that ensures you won't have to use debt later?

You can get the worksheets shown in this recap here:

2019 Budget-by-Paycheck Workbook: Budget-by-Paycheck™ Digital Download

“Where Did My Money Go” Worksheets: “Where Did My Money Go?” Printable Worksheets